Direct answer: For FY 2025-26, most salaried Indians should choose the new tax regime. Choose the old regime only if your old-regime deductions and exemptions are genuinely high, usually above ₹5 lakh to ₹8 lakh depending on your income.

Why this matters now

| Step / Item | What to Know | Details |

|---|---|---|

| New regime comparison | New tax may be better than old tax | Snippet says going with the new tax is better than with the old tax |

| Old regime deductions | Savings may require declarations | Snippet mentions declaring HRA and a home loan in the old regime |

| 30% tax bracket | New regime may be better in most cases | Snippet says people in the 30% tax bracket are better off with the new regime unless having huge deductions |

| Yearly choice | Salaried person can switch every year | Snippet says a salaried person can switch between new and old every year |

| Employer declaration | Choice given to employer may still be changed | Snippet says even if you give your employer new or old, you can switch between regimes |

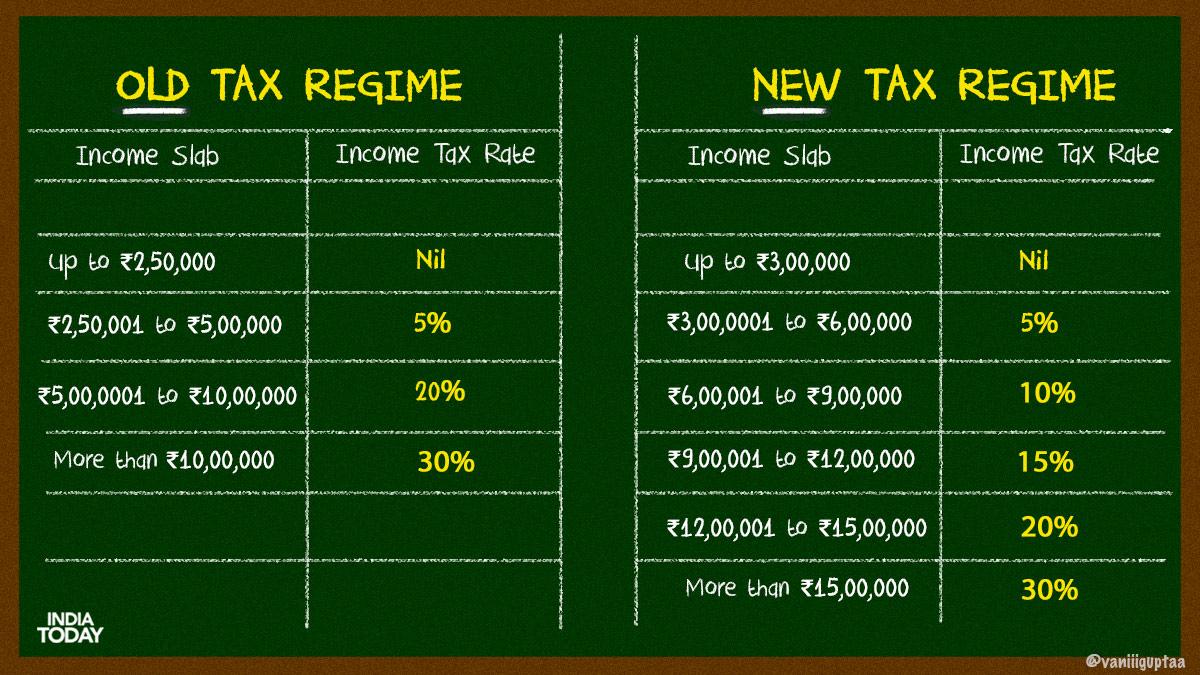

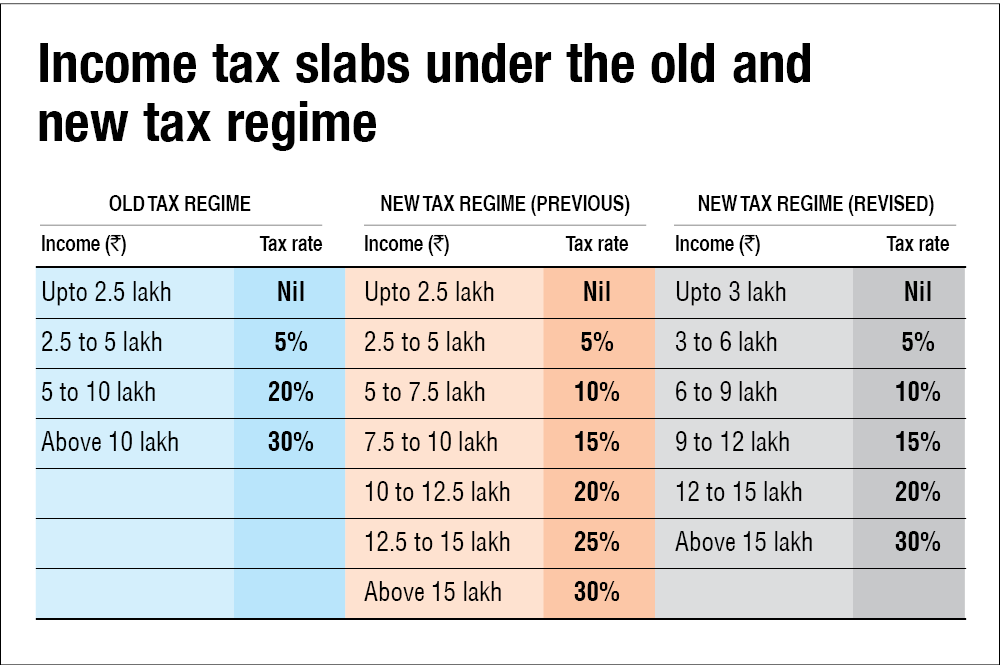

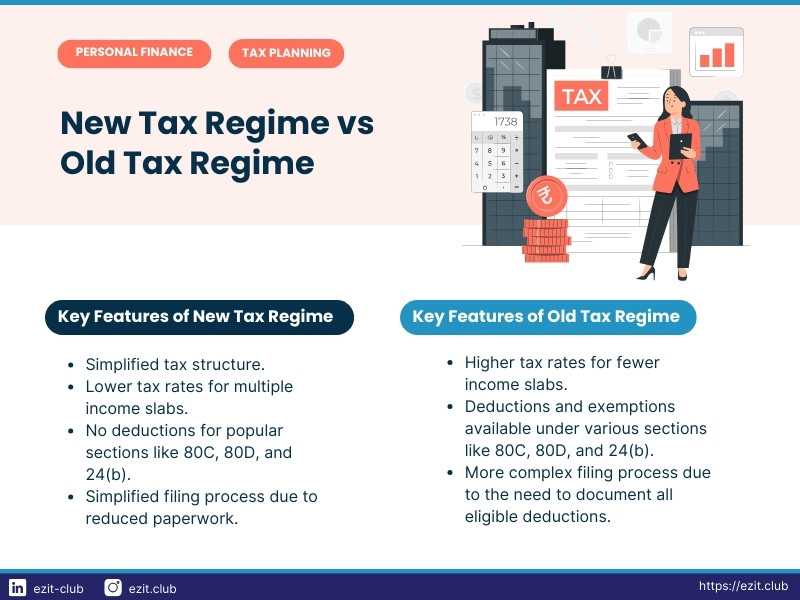

| Exemptions and deductions | Old regime allows more; new disallows most | Snippet says old regime offers a wide range of exemptions and deductions, while new regime disallows most |

The choice became more important after the Union Budget 2025. For FY 2025-26, the new regime has a ₹75,000 standard deduction for salaried taxpayers and rebate benefits that can make salary income up to ₹12.75 lakh tax-free, assuming no special-rate income like capital gains.

This changes the old logic. Earlier, people blindly chose the old regime because it had 80C, HRA, home loan interest and medical insurance deductions. That is no longer smart for everyone. If you are forcing yourself to buy unwanted insurance, lock money in weak investments, or take a home loan only to save tax, you may be losing more than you save.

The honest answer is simple: new regime first, old regime only after calculation. If your salary is moderate and you do not have very high rent or home loan interest, the new regime will usually win. If you want a deeper checklist before filing, read 9 Smart Checks Before Choosing Old or New Tax Regime for ITR Filing 2026.

How to decide in 5 steps

-

Start with your gross salary, not CTC.

Do not use your company CTC blindly. Use taxable salary components from your Form 16 or salary slip. CTC may include employer PF, gratuity, insurance, bonus assumptions and other items that are not taxed the same way. -

Check your income level under the new regime.

For FY 2025-26, the new regime slabs are more generous than before. The key point: salaried taxpayers can get a ₹75,000 standard deduction. So if your salary income is up to around ₹12.75 lakh, the new regime may bring your tax to zero because of rebate and standard deduction, subject to conditions. -

Add only real old-regime deductions.

Count only deductions you can actually prove. Common old-regime items include:- Section 80C: EPF, PPF, ELSS, life insurance premium, home loan principal, children’s tuition fees, up to ₹1.5 lakh.

- HRA exemption: useful if you live on rent and receive HRA from employer.

- Home loan interest: up to ₹2 lakh for self-occupied property, subject to rules.

- Section 80D: medical insurance premium for self, family and parents.

- Section 80CCD(1B): extra ₹50,000 for NPS contribution.

Do not count fake rent, cash donations, or insurance bought only for tax saving. If you cannot defend it with documents, do not include it.

-

Use this rough break-even test.

For many salaried people, the old regime starts beating the new regime only when deductions are large. Roughly speaking:- At ₹12 lakh salary, old regime needs around ₹6.5 lakh of deductions to match zero tax under the new regime.

- At ₹15 lakh salary, old regime may need around ₹5.4 lakh of deductions.

- At ₹20 lakh salary, old regime may need around ₹7 lakh of deductions.

- At ₹25 lakh salary, old regime may need around ₹8 lakh of deductions.

These are broad numbers for salaried taxpayers and can change with exact salary structure. But they show the main point: basic 80C alone is not enough to make the old regime better.

-

Remember that employer declaration is not final.

Many employees panic after selecting the wrong regime with HR. Relax. For salaried people without business income, you can usually choose the final regime while filing your ITR. Your employer selection mainly affects monthly TDS. If extra TDS was deducted, you can claim refund while filing.

Common mistakes and myths

Myth 1: “Old regime is always better if I invest.”

Not true anymore. Suppose you invest ₹1.5 lakh under 80C and pay medical insurance premium. That may still not beat the new regime if your income is in the range where the new rebate and lower slabs help more. Tax-saving investments are good only if they also fit your financial plan.

Myth 2: “People in the 30% bracket should always choose old regime.”

This is also wrong. A person earning ₹25 lakh may still find the new regime better unless they have very high HRA, home loan interest and other deductions. At higher income levels, the old regime needs serious deductions, not small ones.

Myth 3: “If I told my employer one regime, I am stuck.”

For most salaried taxpayers, you are not stuck. You can make the final choice while filing ITR. The only issue is cash flow. If your employer deducted more TDS during the year, your money may come back later as refund. If less TDS was deducted, you may need to pay self-assessment tax with interest if applicable.

One more practical mistake: people compare tax regimes but ignore lifestyle. If you stay with parents and have no rent, no home loan and only basic EPF, the old regime will usually lose. If you live in Mumbai, Bengaluru, Delhi NCR or Pune and pay high rent with proper HRA, the old regime may still be worth checking.

Bottom line — direct recommendation

Choose the new tax regime for FY 2025-26 unless your old-regime deductions are clearly above the break-even point. For most salaried Indians, especially those earning up to around ₹12.75 lakh, the new regime is the cleaner and better choice.

Pick the old regime only if you have a strong combination of HRA exemption, full 80C, NPS, medical insurance, home loan interest and other valid deductions. If your only deduction is 80C or EPF, do not overthink it. The new regime will likely save you money and paperwork.

Before filing ITR in 2026, run the numbers once using your actual Form 16 and AIS/TIS data. For a practical checklist, see 7 Smart Ways to Choose Between Old and New Tax Regime in 2026.

FAQ

Is it better to select old tax regime or new tax regime?

For most salaried taxpayers in FY 2025-26, the new tax regime is better. Select the old regime only if you have large valid deductions, usually from HRA, home loan interest, 80C, NPS and medical insurance.

Is the new tax regime better than the old?

Yes, for most people. The new regime has lower rates, a higher standard deduction for salaried taxpayers and strong rebate benefits. The old regime is better only for people with high deductions and proper documents.

Which tax regime is better for ₹25 lakh income?

At around ₹25 lakh salary, the new regime is usually better unless you have roughly ₹8 lakh or more in old-regime deductions and exemptions. If you have a big HRA exemption plus home loan interest, calculate both before deciding.

Can I switch between old and new tax regime every year?

If you are a salaried person without business or professional income, you can generally choose between the regimes every year while filing ITR. If you have business or professional income, switching rules are more restrictive.

What if I selected the wrong regime with my employer?

For most salaried employees, you can correct the choice while filing your income tax return. Your employer’s choice affects TDS during the year, but the final tax calculation happens in your ITR.

*Affiliate link — we may earn a small commission at no extra cost to you.

Millennial writer covering everyday money struggles, price hikes, and life in India through a Gen-Z lens. Writes the way real people talk — no jargon, just facts.