| City / Bank | Rate or Price | Key Detail |

|---|---|---|

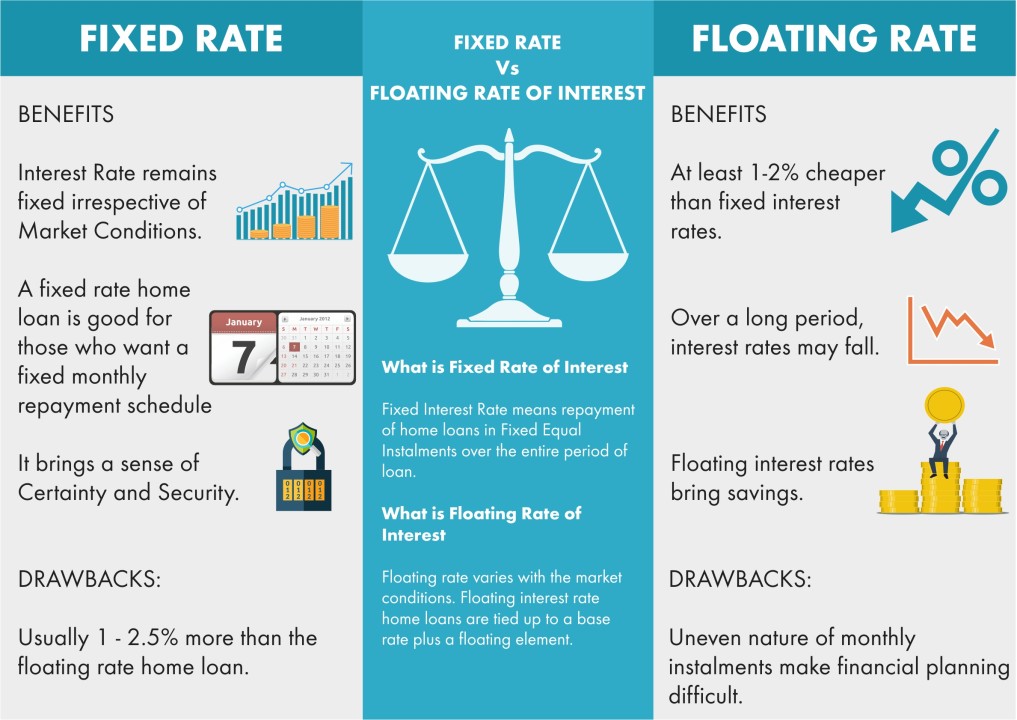

| Fixed rate loans | Slightly higher than floating | Usually priced slightly higher than floating rate loans |

| Floating rate loans | 1–2.5% lower than fixed | Typically lower initially, helping reduce total loan expenses |

| Fixed rate of interest | Stable EMIs | Chosen for certainty and protection from rising rates |

| Floating interest rates | 1-2.5 per cent lower than fixed | Listed as a pro of floating interest rates |

| Floating rate loans | Adjustable rates | Move in sync with the market rate |

A small change in your home loan rate can change your EMI by thousands of rupees. That is why the choice between fixed and floating interest rates is not just a bank formality.

Many borrowers focus only on the lowest rate today. But the better question is: “Can I handle changes tomorrow?”

Fixed vs Floating Home Loan: What It Really Means

What is a fixed rate home loan?

A fixed rate home loan keeps the interest rate the same for a set period, or sometimes for the full loan term. This means your EMI stays predictable.

It is useful when rates are expected to rise. It also helps families who plan monthly budgets tightly and do not want surprises.

What is a floating rate home loan?

A floating rate home loan moves up or down when the lender changes its benchmark rate. Your EMI or loan tenure can change over time.

Floating rates usually start lower than fixed rates. This can make them attractive, especially when the gap between fixed and floating rates is large.

The Key Difference Is Not Just EMI

Most people compare only today’s EMI. That is a mistake. You should also compare risk, flexibility, prepayment plans, and how long you plan to keep the loan.

| Factor | Fixed Rate | Floating Rate |

|---|---|---|

| Starting interest rate | Usually higher | Often lower by about 1% to 2.5% |

| EMI stability | More stable | Can rise or fall |

| Best when | Rates may rise | Rates may fall or stay steady |

| Budget comfort | Good for fixed income families | Good for flexible budgets |

| Long-term savings | Possible if rates rise sharply | Possible if rates stay low or fall |

7 Smart Checks Before You Decide

1. Check the rate gap first

If the fixed rate is only a little higher, it may be worth paying extra for peace of mind. But if the fixed rate is much higher, a floating loan may save more money at the start.

For example, if a floating loan is 8.5% and a fixed loan is 10.5%, the difference is big. You must ask if the safety is worth the extra cost.

2. Look at your income type

If you have a stable salary and strict monthly expenses, a fixed rate can feel safer. Your EMI does not keep changing with market rates.

If your income is growing or you have bonuses, business income, or side income, a floating loan may be easier to manage. You may also be able to prepay faster.

3. Think about loan tenure

For a short loan period, floating rates can work well because there is less time for big rate changes. For a long loan period, both risk and savings can become larger.

A 20-year or 25-year loan will see many rate cycles. So do not decide only by today’s rate.

4. Ask how the bank changes rates

With floating loans, ask which benchmark is used and how often the rate resets. Also ask whether the EMI changes or only the loan tenure changes.

This matters because some borrowers do not notice that their loan tenure has quietly increased. A lower EMI today can sometimes mean more interest later.

5. Check if “fixed” is truly fixed

Some home loans are fixed only for a few years and then become floating. Read the loan paper carefully before you sign.

Ask the lender clearly: “Will this rate remain fixed for the full loan term?” If not, ask when it will reset.

6. Plan for prepayment

If you plan to make part-payments often, check the charges and rules. Floating loans are often more flexible for individual borrowers, but you should confirm this with the lender.

Prepayment can reduce total interest a lot. This is especially useful in the first half of the loan, when the interest part of EMI is higher.

7. Use a calculator, but do not trust it blindly

A home loan fixed vs floating calculator can show the EMI difference. But it cannot predict future rates perfectly.

Use it to test different cases. Try one case where rates rise by 1%, one where they fall by 1%, and one where they stay the same.

When a Fixed Rate Home Loan Makes Sense

A fixed rate is a good choice if you want certainty over savings. It is also suitable if your EMI is already close to your comfort limit.

It can work well when interest rates are low and you expect them to go up. It is also useful for buyers who do not want to track rate changes every few months.

If you are planning to buy soon, you can also compare current market signals in 7 Key Things to Know About Home Loan Interest Rates in India in May 2026. It can help you understand whether rates look costly or reasonable right now.

When a Floating Rate Home Loan Makes Sense

A floating loan is better if you want a lower starting rate and can handle changes in EMI or tenure. It may also suit you if you expect rates to fall or remain steady.

It is popular among borrowers who plan to prepay the loan early. If you reduce the loan balance faster, future rate changes may hurt less.

Before deciding, also look at the full buying picture. Our Complete Guide to India’s May 2026 Property Market: Home Loan Rates, Rent vs Buy, and RERA Checks explains how rates, property prices, and rent decisions connect.

A Simple Step-by-Step Guide

Step 1: Find your safe EMI limit

Do not borrow based on the maximum loan the bank offers. Choose an EMI that leaves room for food, school fees, medical costs, insurance, and savings.

Step 2: Compare fixed and floating offers

Get quotes from at least three lenders. Compare the rate, processing fee, reset rules, prepayment terms, and loan conversion charges.

Step 3: Test a higher EMI case

If choosing floating, check whether you can pay the EMI if the rate rises by 1% or 2%. If that feels stressful, fixed may be safer.

Step 4: Decide based on your risk comfort

If peace of mind matters most, choose fixed. If saving interest and flexibility matter more, choose floating.

FAQ

Which is better: fixed or floating home loan?

There is no one answer for everyone. Fixed is better for stable EMIs, while floating is better for lower starting rates and flexibility.

Are SBI home loans fixed or floating?

SBI home loan products are commonly linked to floating rates, but offerings can change. Always check the latest SBI terms, benchmark rate, spread, and reset rules before applying.

Does HDFC offer fixed or floating home loans?

HDFC and other major lenders may offer different rate types depending on the product and customer profile. Ask whether the rate is fully fixed, partly fixed, or floating from day one.

Why are floating rates usually lower than fixed rates?

Floating loans pass interest rate risk to the borrower. Since the bank is not locking the rate for you, the starting rate is often lower than a fixed loan.

Can I switch from fixed to floating later?

Many lenders allow switching, but there may be charges or conditions. Ask about conversion fees before taking the loan, not after rates change.

Final Recommendation

Choose a fixed rate home loan if your budget is tight, your income is steady, and rising EMIs would cause stress. The higher starting rate can be worth it for safety.

Choose a floating rate home loan if the rate gap is large, your income can handle changes, and you plan to prepay when possible. For most borrowers who can manage some risk, floating often gives better value at the start.

*Affiliate link — we may earn a small commission at no extra cost to you.

Education journalist covering competitive exams, board results, and career transitions in India. Her CBSE and higher education coverage has helped thousands of students navigate admissions.