From 1 January 2026, RBI’s newer prepayment directions make one thing very clear for borrowers: a floating-rate home loan should not trap you with a foreclosure fee. That matters because even one extra prepayment of ₹2 lakh on a large loan can cut months from your loan and save lakhs in interest.

Many borrowers still ask their bank branch, “Will I be charged if I close my home loan early?” The short answer is simple, but the fine print changes if your loan is fixed-rate, mixed-rate, business-linked, or taken as a loan against property.

The 2026 Rule in Plain English

What RBI says for floating-rate home loans

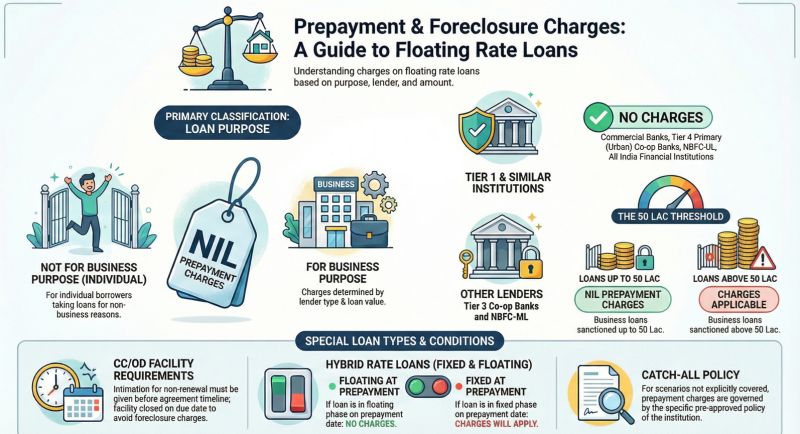

RBI has long protected home loan borrowers from unfair foreclosure charges on floating-rate housing loans. A key RBI instruction from 5 June 2012 stopped banks from charging foreclosure penalties on floating-rate home loans.

RBI later widened this approach. On 2 August 2019, it told regulated lenders not to charge foreclosure or prepayment fees on floating-rate term loans given to individual borrowers for non-business purposes. The newer 2026 framework keeps this borrower-friendly direction strong.

What “zero penalty” really means

Zero penalty means the bank should not charge you simply because you paid early. This applies to both full closure and part-prepayment when the loan is a floating-rate home loan in your personal name.

But the bank may still collect normal dues such as unpaid interest up to the closure date, document retrieval charges if disclosed, or statutory charges. These are not the same as a prepayment penalty.

Quick Data Table: What You May Pay in 2026

| Loan type in 2026 | Prepayment charge position | What to check |

|---|---|---|

| Floating-rate home loan to an individual | 0% penalty | Ask for a zero-foreclosure statement |

| Fixed-rate home loan | May have a charge if written in the agreement | Look at the sanction letter and schedule of charges |

| Dual-rate loan | May be treated as fixed during the fixed period | Check when it changes to floating |

| Loan against property | Rules can differ by purpose and rate type | Check if it is personal or business-linked |

11 Practical Rules Borrowers Should Follow

1. Prepay floating-rate home loans without fear

If your loan is floating-rate and taken for your own home, the bank should not charge a foreclosure penalty. This is the main RBI protection home buyers should use in 2026.

2. Do not assume fixed-rate loans are free to close

Fixed-rate loans are different. The lender may charge a fee if it was clearly written in the loan papers, so read the “prepayment” and “foreclosure” clauses before paying a large amount.

3. Check dual-rate loans carefully

A dual-rate loan starts with a fixed rate and later moves to floating. If you prepay during the fixed period, the bank may apply the fixed-rate rule.

4. Part-prepayment and full foreclosure are not the same

Part-prepayment means you pay extra but keep the loan running. Foreclosure means you close the full loan. For floating-rate home loans, both should be free from penalty for individual borrowers.

5. Ask the bank to reduce tenure, not EMI

If your monthly budget is stable, choose tenure reduction. This usually saves more interest than reducing EMI.

6. Use a simple calculator before paying

Example: On a ₹50 lakh loan at 9% for 20 years, the EMI is about ₹44,986. If you prepay ₹2 lakh after one year and keep the EMI same, you may cut around 22 months and save roughly ₹8 lakh in interest.

7. Get the amount in writing

Before transferring money, ask for a written prepayment quote. It should show principal outstanding, interest up to date, and any other fee separately.

8. Do not confuse processing fee with prepayment fee

A balance transfer to another bank may involve a processing fee at the new lender. That is different from your old bank charging a foreclosure penalty.

9. SBI and other banks must follow RBI

If your SBI home loan, HDFC Bank loan, ICICI Bank loan, or other bank loan is floating-rate and personal, the same RBI rule applies. The logo on the loan statement does not change the rule.

10. Compare prepayment with rate switching

Sometimes, paying a small conversion fee to move to a lower interest rate can save more than one small prepayment. If you are tracking rates, this guide on 7 Key Things to Know About Home Loan Interest Rates in India in May 2026 can help you compare both choices.

11. Keep property plans in mind

If you plan to sell the flat soon, foreclosure paperwork matters as much as interest saving. Before buying or selling, check RERA records, market prices, and loan costs using this Complete Guide to India’s May 2026 Property Market: Home Loan Rates, Rent vs Buy, and RERA Checks.

Step-by-Step: How to Prepay Your Home Loan in 2026

Step 1: Confirm your interest type

Open your sanction letter or loan account page. Find whether the loan is floating, fixed, or dual-rate.

Step 2: Ask for a prepayment statement

Email the bank and ask for a statement that clearly says prepayment penalty: nil if your loan is eligible. Keep this email for your records.

Step 3: Choose EMI reduction or tenure reduction

Pick tenure reduction if your goal is to save interest. Pick EMI reduction only if you need monthly cash relief.

Step 4: Pay through traceable banking channels

Use net banking, cheque, or bank transfer. Avoid cash payments because proof becomes harder later.

Step 5: Collect updated loan schedule

After the payment is posted, ask for the revised amortisation schedule. If closing the loan fully, collect the no-dues certificate and original property papers.

FAQs on RBI Home Loan Prepayment Rules 2026

What is the prepayment rule for RBI home loan 2026?

For individual borrowers with floating-rate home loans, lenders cannot charge a prepayment or foreclosure penalty. This applies when the loan is for personal housing and not for business use.

Where can I download the RBI home loan prepayment rules 2026 PDF?

Use the official RBI website and search for prepayment or foreclosure charge directions. Avoid random PDF links from unknown sites because old circulars and new directions may be mixed together.

Does the RBI rule apply to SBI home loans in 2026?

Yes. SBI is regulated by RBI, so a floating-rate home loan to an individual should not carry a foreclosure penalty. If a charge appears, ask the branch to give the RBI basis in writing.

Can a bank charge penalty on a fixed-rate home loan?

Yes, it may charge if the loan agreement allows it and the fee was disclosed. This is why fixed-rate borrowers should read the schedule of charges before making a large prepayment.

What if the bank still charges me?

First complain to the lender in writing. If it is not fixed, you can escalate under the RBI Integrated Ombudsman Scheme, 2021 through RBI’s complaint portal.

Final Recommendation

If you have a floating-rate home loan in 2026, prepay whenever you have a stable emergency fund and no high-interest debt. Choose tenure reduction, get the zero-penalty statement in writing, and do not delay just because the bank hints at foreclosure charges.

For fixed or dual-rate loans, check the charge first. But for a normal floating-rate home loan, the clear recommendation is this: use RBI’s zero-penalty protection and cut your interest burden early.

*Affiliate link — we may earn a small commission at no extra cost to you.

Personal finance writer with 6+ years covering Indian stock markets, home loans, and tax-saving investments. Previously contributed to MoneyControl and ET Wealth. Based in Mumbai, she helps middle-class Indians make sense of their money.